AI startup funding trends 2025 (US and Nordic regions) show continued mega-round activity in the United States. Nordic markets have shifted from early seed successes to producing billion-dollar scale-ups.

In 2025, the United States matched 2024’s count of startups raising $100 million or more. However, analysts note a higher incidence of companies securing multiple mega-rounds this year.

Meanwhile, the Nordics produced breakout revenue outcomes, exemplified by Lovable’s $200 million first-year performance.

Industry participants note that, in the Nordics, ‘billion-dollar companies’ are now emerging where €1 million once sufficed.

Therefore, investors and analysts should view current flows as strategic reallocation of capital into proven AI scale vectors. Consequently, deal sourcing and due diligence are shifting toward companies with repeatable revenue and multi-round funding histories.

For founders, this means heightened pressure to demonstrate scale and capital efficiency earlier than before. Moreover, cross-border investor interest is increasing, especially from US firms evaluating Nordic product-market fit.

Market factors shaping AI startup funding trends 2025 (US and Nordic regions)

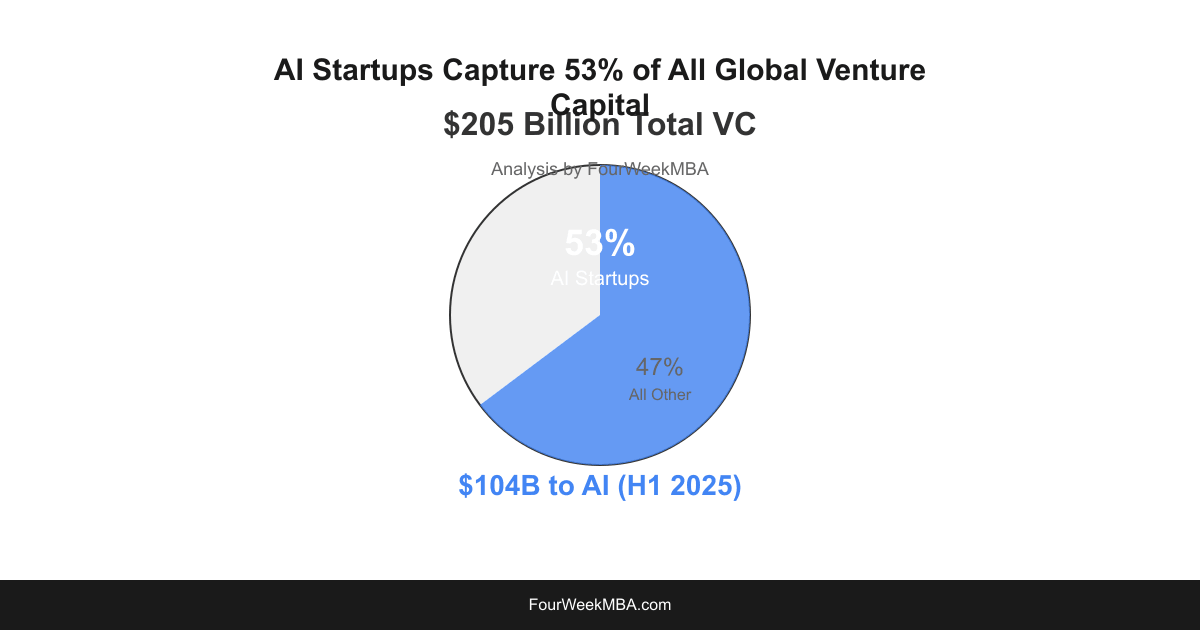

Capital allocation in 2025 reflects concentrated investor conviction and regulatory recalibration, and these forces are steering distinct regional outcomes. Venture capital momentum remains strong in North America, where mega-round activity continues to underpin valuations and liquidity events. According to reporting, North America captured the majority of AI VC flows between February and May 2025, despite a difficult political environment TechCrunch article.

Meanwhile, generative AI and model infrastructure continue to attract disproportionate capital because they promise platform economics and high margins TechCrunch article.

Key market drivers

- Venture capital climate: Fund managers prioritize repeatable revenue and defensible moats, and therefore favor follow-on capital for proven startups.

- Regulatory environment: The EU AI Act imposes tiered obligations, which alters product roadmaps and compliance budgets for European firms EU AI Act enters force.

- Sector focus: Investors concentrate on generative models, MLops, data labeling tooling, and domain verticalization, which create clear exit pathways.

Regional dynamics diverge. In the Nordics, scale-ups like Lovable demonstrated rapid monetization, which has accelerated cross-border interest and valuation uplifts TechCrunch article on Lovable. As one analyst observed, “Last year was monumental for the AI industry in the U.S. and beyond,” and therefore limited capital pools are routing to companies with clear path-to-scale. Consequently, portfolio construction now emphasizes staged capital deployment, stronger governance, and regulatory risk mitigation.

AI startup funding trends 2025 (US and Nordic regions): Strategic implications

Funding concentration in 2025 creates distinct strategic pressures for stakeholders. The United States sustains a high share of mega-round capital, and therefore liquidity and valuation benchmarks remain anchored to large-scale outcomes. According to reporting, North America captured the bulk of AI VC flows in mid-2025, despite political headwinds.

Meanwhile, the Nordics are producing rapid monetization cases that attract cross-border allocators.

For investors, capital allocation now favors repeatable revenue and defensible moats, and therefore follow-on capital is premium. Consequently, portfolio construction emphasizes milestone-based tranche funding, stronger governance, and regulatory scenario planning. Analysts point to generative AI and model infrastructure as primary attractors of capital.

For founders, the bar for late-stage entry has risen. Startups must demonstrate ARR growth, unit economics, and compliance readiness. As one industry commentator observed, “Last year was monumental for the AI industry in the U.S. and beyond,” underscoring investor selectivity.

For policymakers, balancing innovation and risk remains central. The EU AI Act changes compliance costs, and therefore firms must embed regulatory controls early. Consequently, strategic stakeholders should reprice risk, adjust time horizons, and prioritize cross-border diligence.

AI startup funding trends 2025 (US and Nordic regions) confirm concentrated capital allocation and rising investor selectivity. The United States maintains high mega-round activity, matching 2024 in $100 million plus rounds. However, investors increasingly favor repeatable revenue and defensible moats, which drives staged follow-on funding.

Nordic markets show accelerating late-stage checks and faster monetization instances. Rapid monetization appears in cases such as Lovable, which recorded $200 million revenue within its first year. As a result, cross-border capital flows are increasing and regional valuation dynamics are shifting.

Consequently, founders must demonstrate ARR, unit economics, and compliance readiness earlier in their lifecycle. Policymakers should balance innovation with oversight, and investors should recalibrate portfolio construction and due diligence across jurisdictions. As one analyst observed, “Last year was monumental for the AI industry in the U.S. and beyond,” underscoring strategic stakes going forward.

Frequently Asked Questions (FAQs)

What are the primary funding sources for AI startups in 2025?

- Venture capital remains the largest source of institutional funding.

- In the United States, crossover investors and institutional allocators supplement late-stage rounds.

- In the Nordics, regional VCs, corporate investors, and public innovation grants play larger roles.

- Therefore, founders often combine private capital with local grants and strategic corporate deals.

How do funding volumes compare between the US and the Nordics?

- The US leads in absolute funding and mega-round frequency.

- Conversely, Nordic volumes are smaller but accelerating, with more late-stage checks.

- As a result, the US skews toward larger deal sizes while the Nordics emphasize selective scale-ups.

What investment risks should stakeholders prioritize?

- Regulatory risk, model and data liability, and concentration risk top the list.

- Additionally, valuation risk and exit-market cyclicality affect return profiles.

- Consequently, investors must stress-test scenarios and require governance safeguards.

How do policy changes affect fundraising dynamics?

- The EU AI Act raises compliance costs for European firms.

- Meanwhile, US policy remains fragmented across states and agencies.

- Therefore, regulatory preparedness now factors into valuation and deal terms.

What should founders prioritize to attract capital?

- Founders should demonstrate ARR growth, unit economics, and repeatable revenue models.

- Moreover, they must embed compliance, strong governance, and clear go-to-market plans.

- Consequently, capital providers reward measurable traction and regulatory readiness.